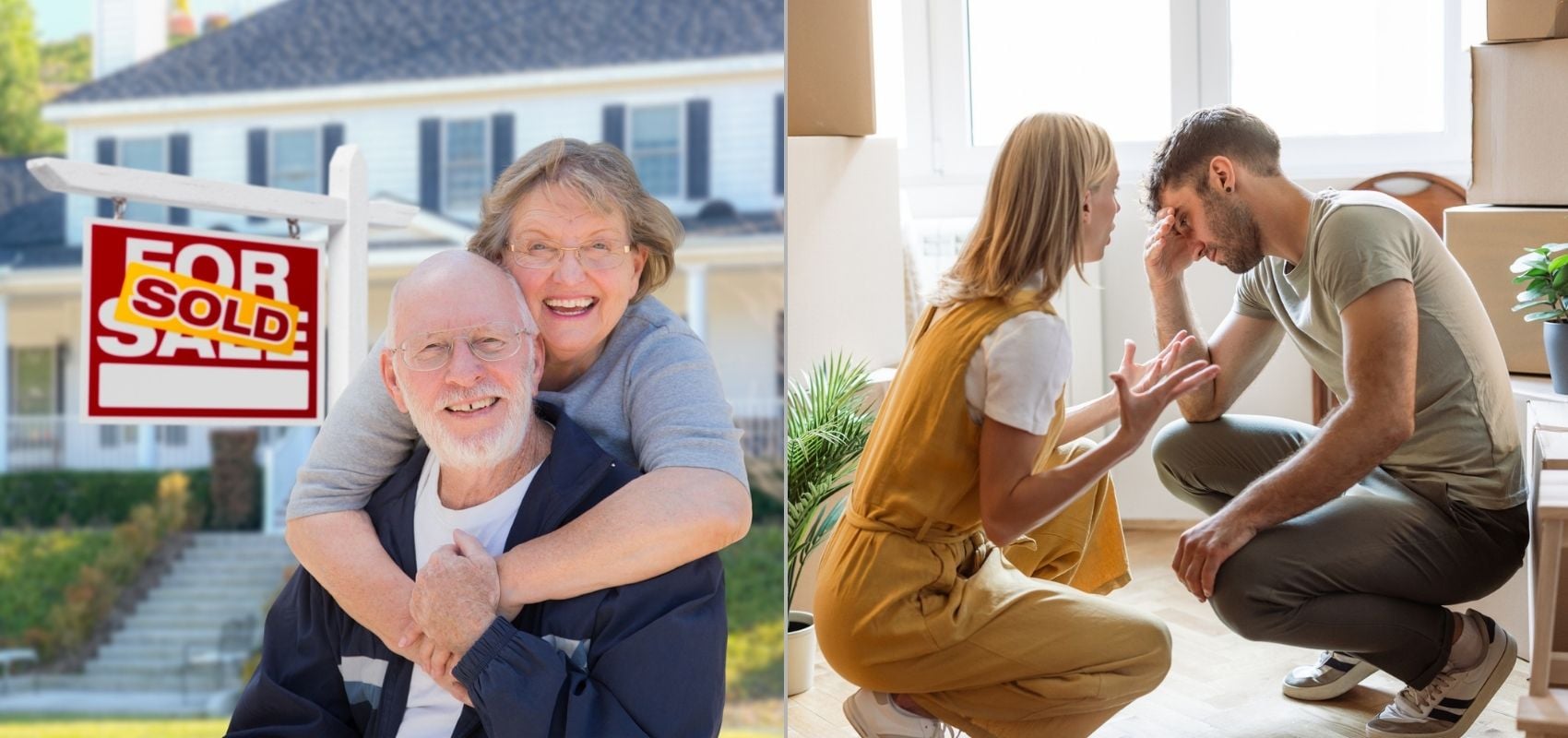

When I heard the price the retired man was asking for his home, a full $80,000 over online estimates of its value, I flinched. The market is hot in our small town, and the location was good, but was it that good? More importantly, would the bank appraise it so high? Just seven years ago, this seller had purchased the home for less than half the price he wanted for it in 2026.

My husband and I were in a spot familiar to many in our generation: trying to scrape together enough cash to buy a house from an older couple, who neither needed nor wanted the space, yet priced it extraordinarily high. Another retiree in our neighborhood recently listed his home, a three-bedroom house with a modest yard, at $100,000 over its estimated value. A third home in town has been relisted at least twice, as the retired woman selling it refuses to lower the price, despite knowing the home needs thousands of dollars in mold remediation and electrical updates. When we offered a number below her asking price, and above the home’s estimated value, she accused us of trying to fleece an older woman. It has since remained on the market for more than a hundred days, but she’s not in a hurry. She owns the home outright.

As the average U.S. home-price-versus-income ratio nears record highs, and home turnover hits record lows, it is hard for young Americans like us to view the possibility of a housing market correction without some sense of justice. Many, both Zoomers and Millennials, believe President Trump ought to do something to force this correction, and bring down the price of a starter home, which has implications for family formation, fertility rates, and the general success potential of young Americans. Pursuant to this, in January, Trump directed the federal government to favor small investors over large institutional ones—single families over Blackstone, for example—in the purchase of single-family homes. Likewise, the White House has successfully lobbied Congress to ban Wall Street investors from buying single-family homes, one of the key provisions of the 21st Century ROAD to Housing Act passed by the Senate in March. The bill, which heads to the House for final approval, also offers a number of changes, from deregulation to building incentives, in an attempt to boost the overall housing supply.

At the same time, Trump has expressed an unwillingness to drive down housing prices for current homeowners, seemingly contradicting his rhetoric on affordability. This is hardly surprising. Trump, not to mention a powerful plurality of Congress members, faces strong incentives against reducing home prices. As long as Boomers hold nearly half of U.S. real estate wealth, any reduction in price hits their pockets directly.

Boomers also hold roughly 51 percent of all U.S. household wealth, more than $85 trillion in assets, which means it is not merely in homeownership that they hold a major advantage over young Americans. The path to financial freedom is undeniably harder for young Americans today than it was for Trump and others of his era. This is due not to youthful discontent, or to exorbitant DoorDash expenses, but to real changes in the economic landscape. One metric economists use to demonstrate the change is the disparity between median annual wages and median home prices. As writer Tom Owens explained in 2024, whereas “the cost of housing has tripled and the cost of transportation has almost doubled, salaries are only up 58% in nominal terms.” Owens compiles what he calls the “Life Difficulty Index,” which is calculated from the median home price, the median household income, and the cost of a Toyota Corolla (a stand-in for modest, reliable transportation) in a given era. By Owens’s metric, the life difficulty index of the average Boomer was 3.47. For the average Gen Xer, it was 3.64. Gen Z clocks in at 5.14, or 7.61 if you factor in the cost of college. Which is to say, not only is getting ahead getting more difficult for each generation, but it is doing so at an accelerating pace.

These numbers give a rough picture: National home price averages skew far higher than the price of housing in economically depressed markets, such as many parts of the rural Midwest. Still, job opportunities are typically few in such markets, which means that moving to a depressed market to buy your first home is a solution for some, but not all.

Comparing census data from 1982 to 2024, journalist Declan Leary notes that the rate of young American homeowners has dropped between 5 and 10 percent across varying age groups since 1982. “The only age group that has a higher rate of homeownership today than in 1982 is those over 65,” Leary writes. Importantly, a mere 3 percent of all single-family rental homes, and less than one half of 1 percent of all single-family homes, are owned by the large corporations like Blackstone that Trump’s executive order in January singled out. The rest are simply owned by Boomers.

Russ Greene has coined the phrase “Total Boomer Luxury Communism” to capture the prickly reality that the U.S. government, especially in its entitlement programs, “redistributes wealth from younger families and workers to seniors, who are on average much richer.”

“Our nation’s policies are heavily biased toward keeping seniors in homes that are more spacious and nearer to major employers than they would otherwise be,” wrote Greene last December. Over the phone, he described how Total Boomer Luxury Communism is affecting housing for the younger generation: “In almost every location in America, there is some sort of special privilege for senior citizens designed to keep them in their housing: deferral programs, assessment freezes, and other special tax breaks.”

As one example, Greene pointed to Proposition 13, a 1978 California constitutional amendment that capped annual property tax-assessment increases and tax rates. While Prop 13 does not advantage senior citizens explicitly or in theory, Greene explained that it does so in practice: People who have purchased homes recently must pay 10 to 20 times the property taxes of those who have owned their homes for longer, a disparity that has the effect of keeping California real estate ownership old. Michigan property taxes have worked in a similar way for years, but that did not stop Governor Gretchen Whitmer from proudly proposing $90 million in property tax cuts for Michigan seniors on February 8.

Perhaps most notable among the effects of this price-to-income disparity is the effect on fertility. Greene tells me:

Location, for younger families, is very important. They want to move where the jobs are, and they want to live in safer neighborhoods with good schools where they can raise their kids. These policies that restrict new housing or keep seniors in their homes longer artificially, they are keeping seniors not just in homes but in particular locations longer. You have empty nesters, retired with no kids around, who have no need for a third or fourth bedroom, living in the nicest, safest, most convenient neighborhoods, closest to work, in Northwest Washington, D.C.

For Greene, an important piece of the puzzle is Social Security, Medicare, and Medicaid expenditures, which in some cases add up to much more than a retirement safety net. Many seniors get to spend their benefits on golf balls, social club memberships, or horseback riding lessons, or pocket $3,000 to $4,000 per month. “You cannot make life affordable for young families and also young workers while also keeping this incredibly expensive and wasteful system,” Greene says.

Mercatus Institute scholar Kevin Erdmann suggests that rising home prices in America are an indication of national poverty, not wealth. Such prices have been achieved through supply restrictions, such as zoning, which slow the construction of new housing. Floor plan designer Bobby Fijan, together with Riley Meik, Harris Rothaermel, and William Davis, seeks to address this problem with a new housing start-up, the American Housing Corporation. Its purpose: to bring back the American row home—filling out what some call the “missing middle” in housing options—and make housing that is tailored to young American families.

“We’re building two and three story, attached, high-quality row homes,” Fijan told me.

One hundred years ago, this would have been the type of product that was built in Brooklyn, in Baltimore, in Georgetown, in South Philly, wherever people were building for working class families. We’re building units between 1,200 and 1,600 square feet, between two and four bedrooms, with the goal of designing them so they work for families with young kids.

Fijan builds his prefabricated townhomes in Austin, Texas, and plans to branch out to other parts of the West within the year, selling individual units and groups of units, and possibly renting in the future. He is careful to note that urban townhomes are not a replacement for single-family homes. Rather, they provide an option for young Americans who are ready to start a family but cannot afford to move to the suburbs, whether because of the price of a single-family house or because of the distance from work.

“It is undeniably true that your built environment shapes you and shapes the things around you,” Fijan said.

I think it filters down to floor plans. If you look at the floor plans of a typical two- or three-bedroom apartment, for example, all the bedrooms are the same size. I don’t know a single family who thinks the master bedroom should be the same size as the two-year-old’s room. If every bedroom is the same size, with an en suite, walk-in closet and master bath, it is designed for roommates. I don’t think anyone is trying to discriminate against children, and yet, it does. It would be a mistake to say families don’t want to live in urban areas. No, families just don’t want to live in this.

The American Housing Corporation offers a practical solution to steep housing prices for young Americans, one that may alleviate pressure on the single-family home market. It is a positive vision that avoids the zero-sum price battles between Boomers and Zoomers.

Another positive vision comes, however circuitously, from the Trump administration, on the issue of immigration. If the tension is between raising property values and lowering prices, fixing illegal immigration accomplishes both indirectly, by decreasing demand for housing and increasing the supply of safe neighborhoods. Successful border policing is a long game, but perhaps the most important one when it comes to family-friendly housing markets. It is an issue Trump and both demographic extremes of his voter base can agree upon.

Ohio businessman Justin Powell offers a third option: Boomers should start passing on wealth now, not later. Powell lobbies for parental generosity, not only because of the time-value of money, but also because it keeps mom and dad involved in their children’s lives.

“Giving early is not just an act of generosity; it is an act of participation,” Powell explained to me.

The idea that “a blessing delayed is a blessing lost” reflects the reality that money has leverage at different stages of life. When giving happens early, the recipient is helped at a pivotal moment, and the giver receives a rare gift as well: the chance to watch that help compound into confidence, stability, and opportunity.

Powell’s solution touches on something beyond fairness. Intergenerational dependence is exactly what Social Security and other benefits programs did away with, intentionally or not. As Boomers receive a large cut of Zoomers’ paychecks in a system all but guaranteed to collapse before Zoomers see a dime, the undeniable effect has been to distance the elderly from their natural sources of support—their children and grandchildren—and even strike enmity between them.

Total Boomer Luxury Communism, and the price of the single-family home, are here to stay as long as retirees retain ownership of the economy. Millennials and Zoomers are in their era of family formation right now. Of those to whom much is given, much is required.