I have boundless regard for Paul Volcker, but the proposed restrictions on bank proprietary trading are, well, fixing the barn’s roof after the horse has bolted. The Obama administration really,really doesn’t get the joke. The banks went bankrupt by loading up on supposedly ultra-safe, AAA-rated assets, spawned out of the derivatives hatcheries with the collusion of corrupt rating agencies (who made most of their money rubber-stamping these time bombs). They did NOT, NOT, NOT blow up taking risky proprietary bets. Yet the rating agencies (who claim no liability for mis-judgments on the grounds that they are exercising the same Constitutionally-protected free speech as a newspaper editorialist!) are in charge of rating credit quality.

The credit crunch keeps crunching along:

1) Commercial and industrial loans at US banks are down 20% year on year;

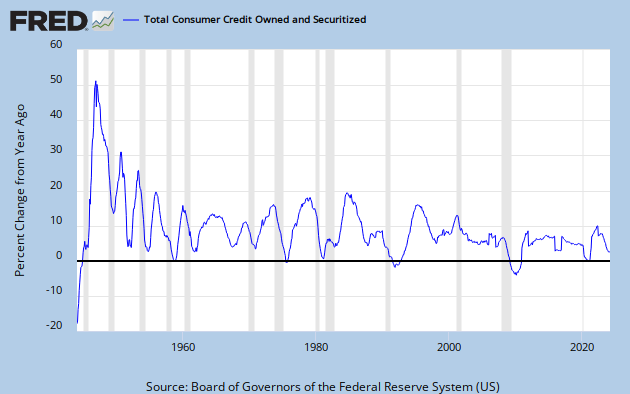

2) Consumer credit fell in November by the largest amount on record, and has fallen year-on-year by the largest proportion since World War II:

3) Commercial paper outstanding has fallen by half

What we have is a Japanese-style banking system in which the banks do nothing but borrow money at close to 0% from the federal government and lend it back at 1% for two years. And that means a “lost decade” along the lines of Japan during the 1990s. There are huge problems in the banking system but this is not the way to fix them.

Proprietary trading is what SAVED the banking system earlier this year. I laid this out in advance exactly a year ago — on Jan. 23, 2008 — in an essay for Asia Times entitled, “Fixing the bank crisis is the easy part.” I wrote:

Today’s problem is far worse than the previous two system insolvencies, to be sure. It is so large that nationalization the banking system very well might crush the credit of the United States. But with close to zero-percent funding from the Federal Reserve, American banks can acquire cheap assets that pay yields of 15%-20%. The cash flow available on non-agency mortgage bonds, credit card bonds, structured bonds backed by corporate loans, and other high-yielding assets is big enough to provide banks with positive cash flow despite mounting losses on real estate, mortgages and consumer loans.

At that point credit markets had broken down, as I observed:

What has happened, rather, is that the market’s willingness to buy credit-sensitive American bonds has collapsed. Between the first quarter of 2007 and the third quarter of 2008, mortgage-backed securities issuance dropped by roughly half, corporate bond issuance by three-quarters, and asset-backed issuance by more than nine-tenths.

$US bn Municipal Treasury Mortgage Related Corporate Agency Asset Backed Q107 107.6 188.5 540.4 305.6 265.4 323.2 Q2 123.6 184.4 628.2 345.8 234.1 329.1 Q3 93.4 171.1 485.4 239.4 185.8 139.3 Q4 104.7 208.3 396.3 236.7 256.5 110.0 Q108 85.0 203.8 391.5 213.1 432.4 59.7 Q2 144.5 219.8 437.8 333.3 387.9 69.7 Q3 89.6 244.8 286.6 82.6 198.8 23.5

The banks earned outsized cash flows by stripping the dead on the battlefield through an enormous proprietary bet. If they hadn’t done so, the economy would be in far worse shape than it is now.

The banks have government support and deep pockets, and can afford to step in when everyone else is in full-tilt panic.

If you want to limit proprietary risk, there are several obvious things to do:

1) Limit the amount of risk banks can take on their books (through Value at Risk and similar models)

2) Take into account the embedded leverage in derivatives as well as actual balance-sheet leverages. This requires modeling, but there are thousands of unemployed hedge fund risk managers who know how to do this, and the models are fairly generic

3) Fix the ratings system. This is an area in which the enormous Fed staff of academics might do a better job than Moody’s, S&P and Fitch, who have lost a great deal of credibility.

The Federal Reserve allowed the banks to put on massive off-balance-sheet leverage during the lead-up to the banking crisis, through Special Investment Vehicles and such like. The regulators simply can take a more conservative approach to leverage.

All this is sensible. But the idea that one can separate proprietary from customer trading is silly to begin with, and undesirable in the extreme. When there’s panic, you want the banks to take proprietary risk as the buyer of last resort.

You have a decision to make: double or nothing.

For this week only, a generous supporter has offered to fully match all new and increased donations to First Things up to $60,000.

In other words, your gift of $50 unlocks $100 for First Things, your gift of $100 unlocks $200, and so on, up to a total of $120,000. But if you don’t give, nothing.

So what will it be, dear reader: double, or nothing?

Make your year-end gift go twice as far for First Things by giving now.